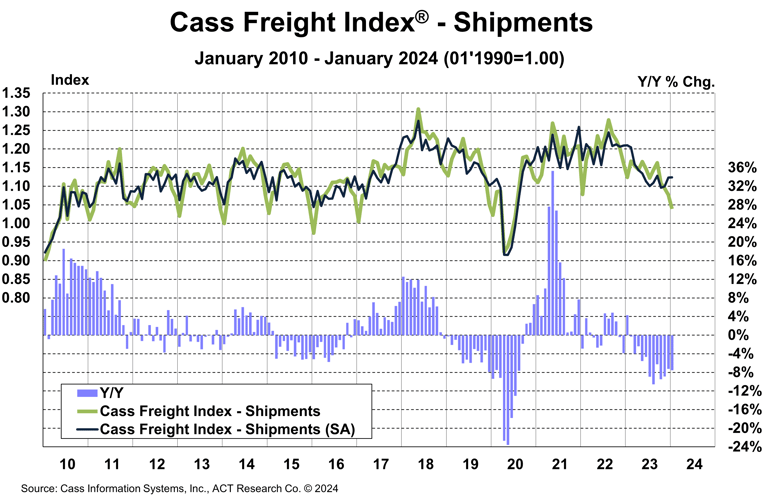

The shipments component of the Cass Freight Index® fell 3.5% m/m in January but was consistent with December in seasonally adjusted (SA) terms. So, despite the harsh weather impact, the January decline was in line with normal seasonality. Freight transportation is, of course, an outdoor sport, and it’s tough to say with precision if this January was worse than most, but if so, the underlying trend in freight improved in January.

After rising 0.6% in 2022, the Cass Shipments index declined 5.5% in 2023. With normal seasonality, this index would be up 5% m/m in February, leaving it down about 6% y/y.

See the Methodology for the Cass Freight Index

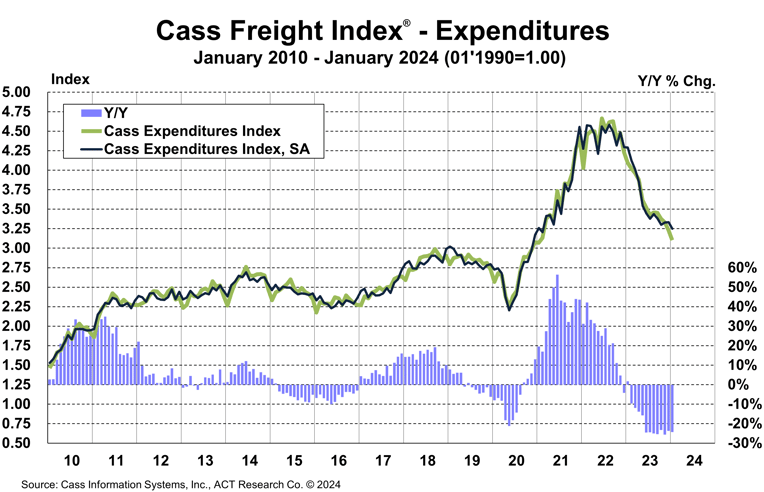

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, fell 4.0% m/m and 24% y/y in January.

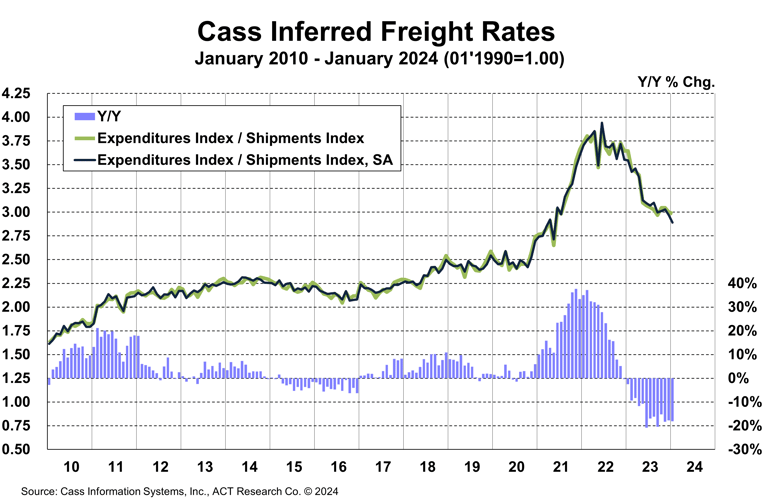

Against a slightly smaller decline in freight shipments (-3.5% m/m), we can infer that overall paid rates were down 0.5% m/m in January (see our inferred rates data series below).

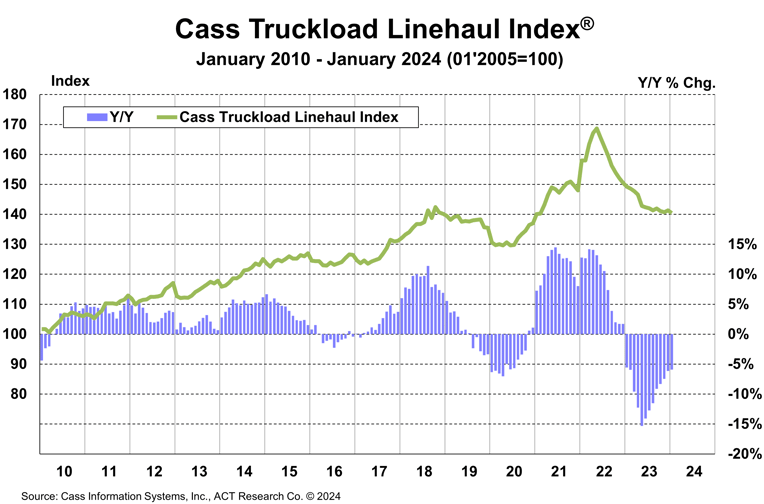

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

U.S. freight spending, as measured by the expenditures component of the Cass Freight Index, fell 19% in 2023, after a record 38% surge in 2021 and another 23% increase in 2022. It’s set to decline about another 16% in 1H’24, assuming normal seasonal patterns from here.

The rates embedded in the two components of the Cass Freight Index declined 18% y/y in January and have now declined 15%-21% for eight straight months.

The normal seasonal pattern from here would put inferred rates down 13% y/y for 1H’24, of which lower fuel prices still account for a few percentage points.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

Stability continued for the Cass Truckload Linehaul Index in January, with a 0.6% m/m decline after rising by 0.4% m/m in December. The 5.9% y/y decline was the narrowest in the past year.

See the Methodology for the Cass Truckload Linehaul Index

While trucking demand remains soft overall, rising import and intermodal trends are key leading indicators of a recovery in trucking this year. Global ocean shipping disruptions will likely add to U.S. freight movements in 2024 as shippers seek to buffer safety stocks.

The U.S. economy also continues to provide upside surprises, and far from heading into a recession, the main concern is the economy running too hot right now, with inflation concerns recently returning to the forefront. The concern that global disruptions could add to inflation falls mostly outside this domestic data set, but the domestic market, which is the much larger piece of U.S. logistics costs, continues to decisively reduce inflation pressure.

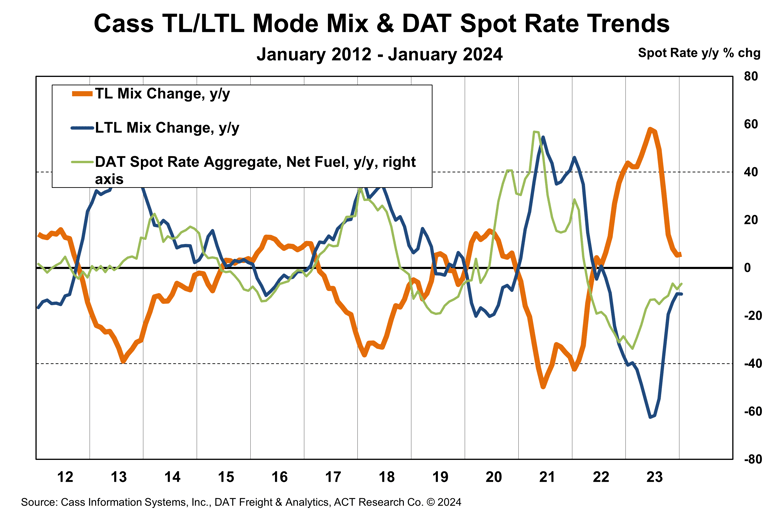

Finally, we check in with the TL and LTL modal mix trends in the Cass database for an update on where we are in the cycle. The chart below demonstrates the cyclicality of modal mix, as LTL mix rises in tight freight markets, and vice versa. Directionally, this suggests the rebalancing is nearing completion.

Our outlook through 2025 is detailed in the ACT Research Freight Forecast. This service provides in-depth analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type, LTL, and intermodal price indexes. We provide monthly, quarterly, and annual predictions for over 40 data series over a two- to three-year time horizon, including capacity, volumes, and rates. The ACT Research Freight Forecast is released monthly in conjunction with the Cass Transportation Index report.

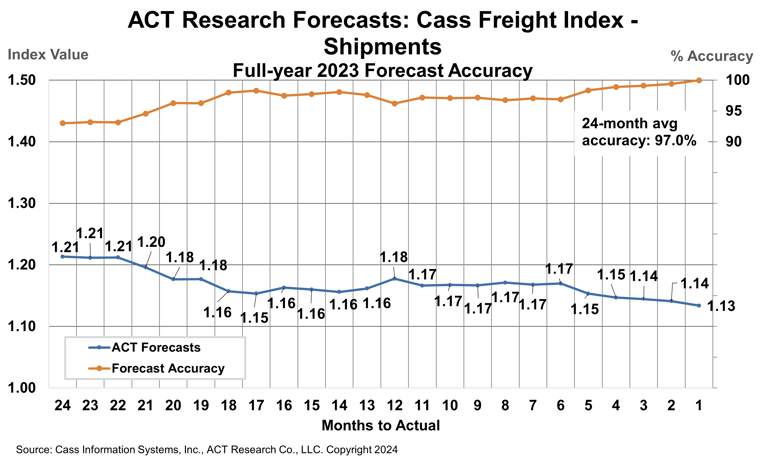

How have ACT Research’s freight forecasts performed? For 2023, ACT’s forecasts for the shipments component of the Cass Freight Index were 96.9% accurate on average for the 24-month forecast period.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

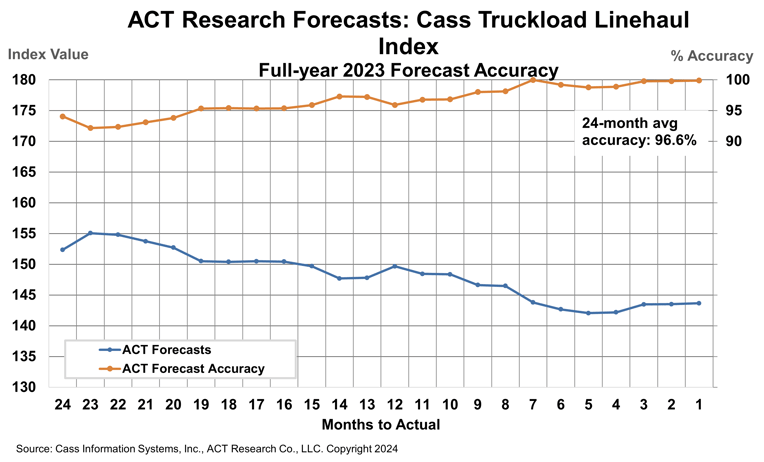

ACT Research’s 2023 forecasts for the Cass Truckload Linehaul Index were 96.6% accurate on average over the past 24 months, and 98.5% accurate over the past 12 months. The Cass Truckload Linehaul Index averaged 143.8 in 2023, precisely in line with our July 2023 estimate.

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.