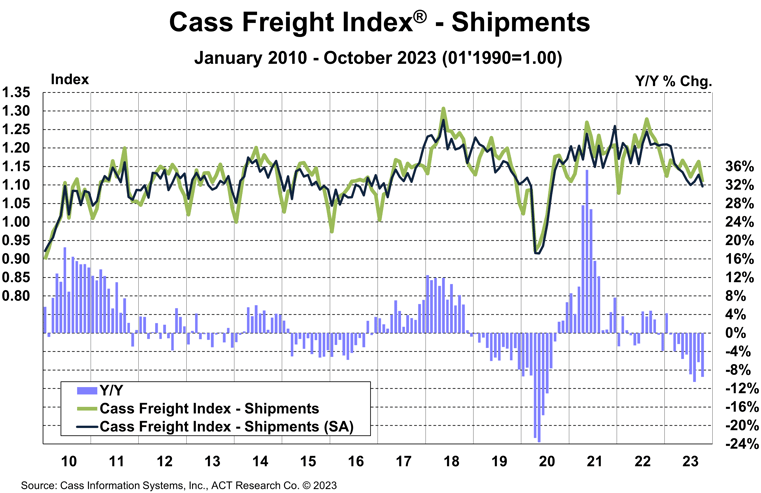

The shipments component of the Cass Freight Index® fell 4.7% m/m in October, more than reversing the past two months of gains to reach a new cycle low. We note this data set includes automotive, so the UAW strike may have had an impact this this month, which suggests a rebound in the months to come.

The 2023 peak season is off to a muted start, but we think overall freight volumes are better than those in the for-hire sector measured by Cass data, as private fleet insourcing persists.

With normal seasonality, this index would be down slightly m/m in November and about 9% y/y.

See the Methodology for the Cass Freight Index

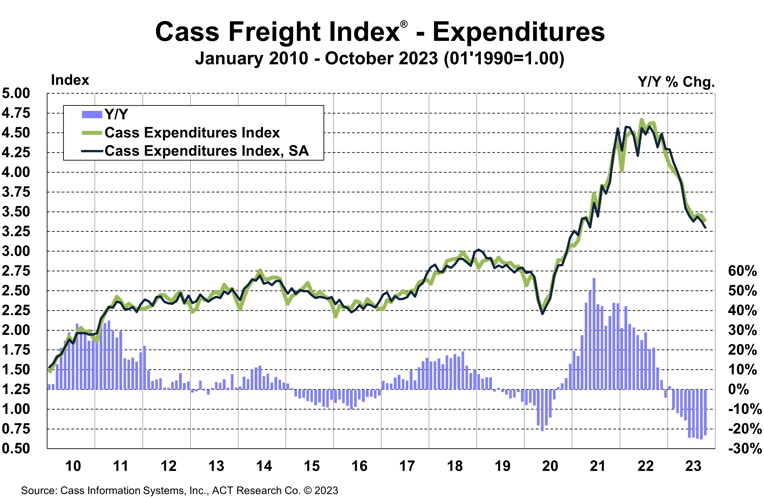

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, fell 2.2% m/m and 23% y/y in October.

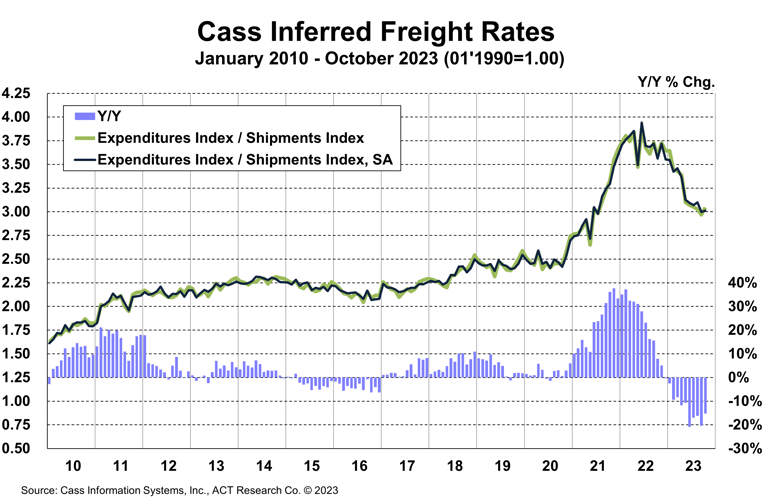

With shipments down 4.7% m/m, we infer rates were up 2.6% m/m in September (see our inferred rates data series below).

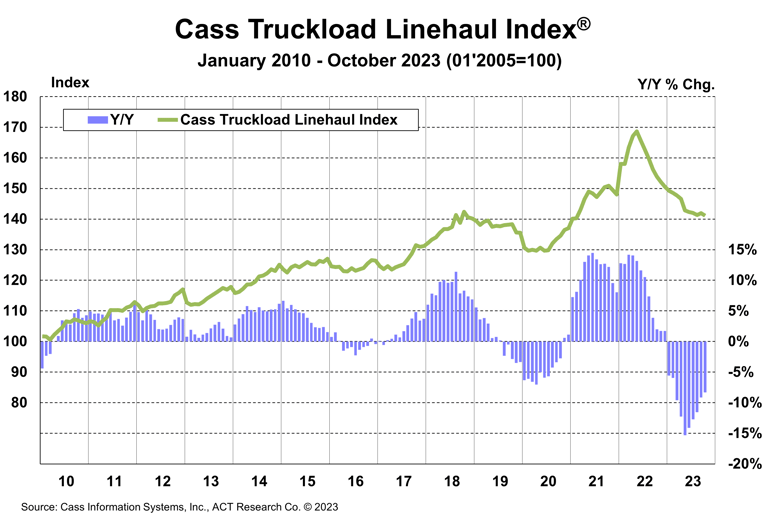

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index rose 23% in 2022, after a record 38% increase in 2021, but is set to decline about 18% in 2023 and another 14% in 1H’24, assuming normal seasonal patterns from here. Both freight volume and rates remain under pressure at this point in the cycle.

The rates embedded in the two components of the Cass Freight Index declined 15% y/y in October, after falling 20% in September.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index fell 0.6% m/m in October to 141.1, after a 0.5% m/m increase in September.

See the Methodology for the Cass Truckload Linehaul Index

We continue to expect modest y/y growth in consumer spending this holiday season, driven by the acceleration in real disposable incomes and the ongoing strong labor market. The recent easing in oil prices improves our confidence that peak season will end on a higher note.

But general economic conditions remain better than those in the for-hire freight market. Although private fleet capacity expansion continues to pull freight from the for-hire market, we think equipment purchasing patterns are changing, which should propel the cycle forward in 2024, even if the broad economy slows.

Our outlook for freight markets to keep bouncing along the bottom in the near term, followed by some holiday volatility and a change in trajectory next year, is detailed in the ACT Research Freight Forecast. This service provides in-depth analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type, LTL, and intermodal price indexes. We provide monthly, quarterly, and annual predictions for over forty data series over a two- to three-year time horizon, including capacity, volumes, and rates. The ACT Research Freight Forecast is released monthly in conjunction with the Cass Transportation Index report.

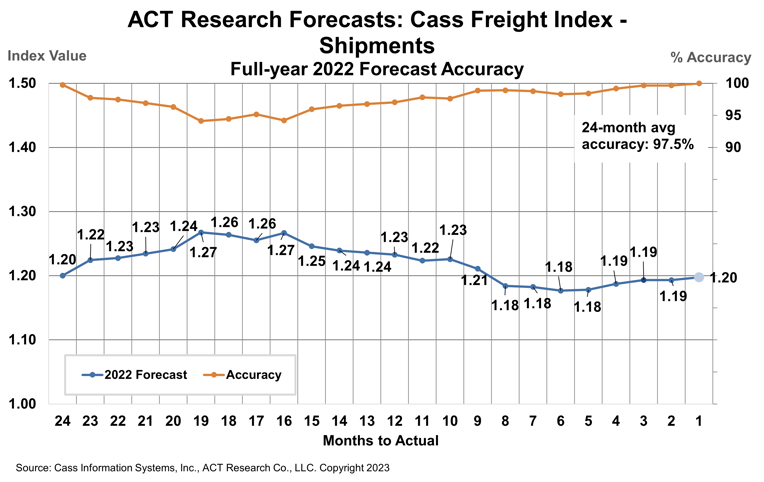

How have their forecasts performed? For 2022, ACT’s forecasts for the shipments component of the Cass Freight Index were 97.5% accurate on average for the 24-month forecast period. Our January 2021 forecast, two full years out, was 99.8% accurate.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

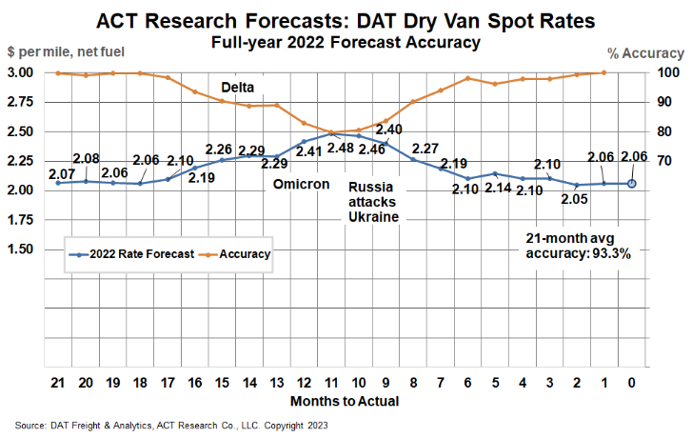

ACT Research’s full-year 2022 DAT spot rate forecasts were 99.7% accurate from Q2’21 (19-21 months out) for dry van and 98.5% for reefer. DAT dry van spot rates, net fuel, finished 2022 at $2.06 per mile, in line with our forecasts to the penny from 18 and 19 months out (June and July 2021).

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.