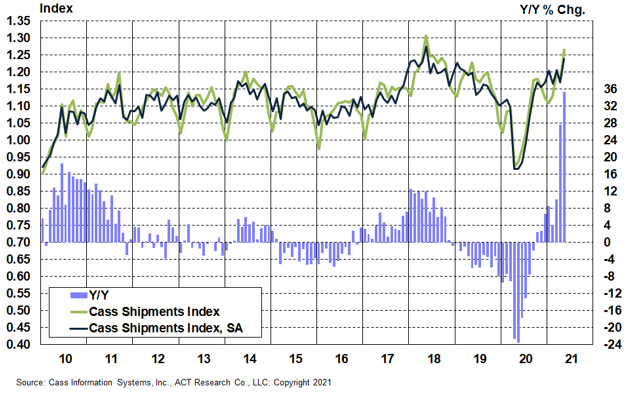

The shipments component of the Cass Freight Index® grew at a record 35.3% y/y pace in May, accelerating from a 27.6% y/y increase in April. It’s safe to say the pandemic recovery is progressing much faster than the recovery from the Great Recession.

A very strong y/y result was expected against an easy comparison amid the pandemic shutdown, but the acceleration was ahead of expectations against a similar comp to April.

Some of the acceleration likely continues to be noise related to the February polar vortex, but it more than reversed the 3.1% m/m decline (SA) in April. Auto production recovered a bit in May, with motor vehicle volumes on the railroads up about 4% m/m in May, although semiconductors remain a major challenge. With containership backlogs in the San Pedro Bay whittling down slower than expected despite amazing port throughput, the May surge in the Cass shipments index was also likely due to a step up in demand for inventory restocking following the recent jump in retail sales.

Chart: Cass Shipments Index, January 2010 – May 2021 (01’1990=1.00)

See the methodology for the Cass Freight Index.

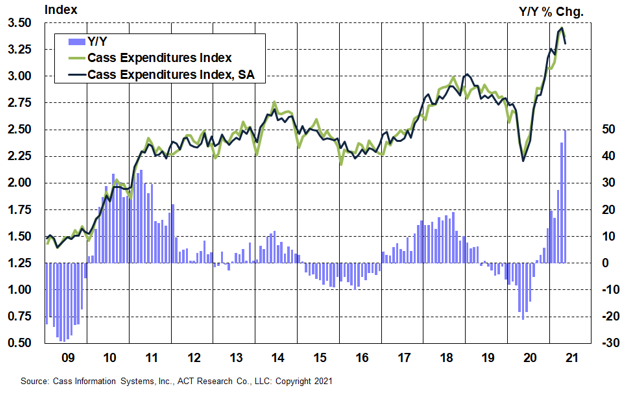

The expenditures component of the Cass Freight Index grew at its fastest pace ever on a y/y basis in May, up 49.9% y/y, accelerating from 45.1% y/y growth in April. As May faced the easiest comparison of the pandemic quarantine period, tougher comparisons in the coming months will slow these y/y increases essentially regardless of freight fundamentals.

On normal seasonal patterns, the easier comparisons would suggest y/y growth at about 45% in June, then slowing to more like 30% y/y growth rates in Q3.

On a seasonally adjusted basis, the expenditures index fell 4.2% from April, and with volumes stronger m/m, the decline was more than explained by lower implied rates (see below), which fell 7.8% m/m. The ACT Freight Forecast report this month fixates quite a bit on the timing of the peak of the rate cycle, but we don’t think this is it.

Chart: Cass Expenditures Index, January 2009 – May 2021 (01’1990=1.00)

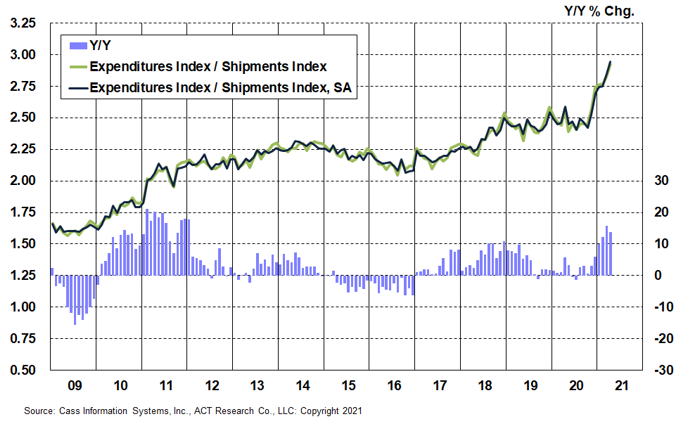

A simple calculation of the Cass Freight Index data (expenditures divided by shipments) produces a data set of “implied freight rates” that explains the overall movement in rates.

Last month, we discussed our expectation that this series would slow with most annual contract freight having been repriced at this point. However, the significant m/m drop was not likely due to market conditions, which by most accounts, including the Cass Truckload Linehaul Index®, continued to increase in May. Rather, our sense is the modal mix within the index was the cause of the slowdown. We should see reconvergence with the stronger Truckload Linehaul Index® as these mix shifts eventually wash out.

This data series is diversified among all modes, with truckload representing more than half of the dollars, followed by rail, LTL, parcel, and so on.

Chart: Cass Implied Freight Rates, January 2009 – May 2021 (01’1990=1.00)

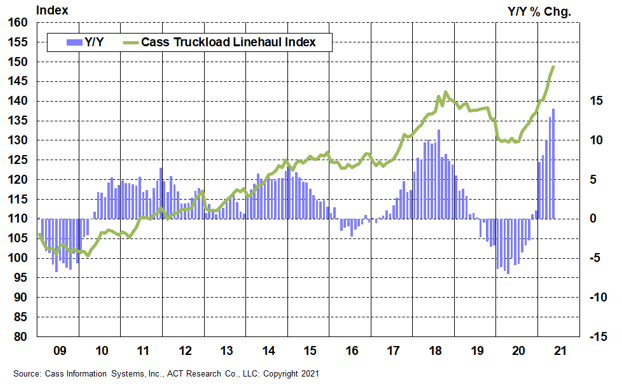

The Cass Truckload Linehaul Index® value of 149.0 in May represented a third consecutive all-time record and accelerated to a 14.1% y/y increase from a 13.0% y/y increase in April. On a m/m basis, the seasonally adjusted index was 1.7% higher than March, in the eleventh straight increase.

With strong freight demand and ongoing supply constraints in both of the critical components of trucking capacity (drivers and tractors), the trend of the Cass Truckload Linehaul Index should remain up and to the right in the near-term. Parts shortages continue to limit truck, trailer, and chassis production, keeping freight markets tight, but equipment fleet growth will improve as the year progresses.

For those who follow this closely, the ACT Freight Forecast report has introduced forecasts for the Cass Truckload Linehaul Index through 2023 (note: forecasts are made solely by ACT Research).

Chart: Cass Truckload Linehaul Index®, January 2009 – May 2021 (01’1990=1.00)

See the methodology for the Cass Truckload Linehaul Index.

Even with considerable supply constraints, the freight cycle is in high-growth mode. While y/y comparisons will naturally slow going forward, the freight markets continue to benefit from a very strong retail economy, very tight inventories, and a backlog of containerships still anchored in the San Pedro Bay.

In addition, while the industrial sector continues to struggle on a relative basis, U.S. capital goods orders have recently broken through a generational ceiling. We believe this portends an unprecedented U.S. capex boom.

So, even as federal stimulus effects fade and consumer spending gradually reverts back to services from goods, the extraordinarily strong U.S. freight recovery across the network in 2021 also has longer-term growth drivers.

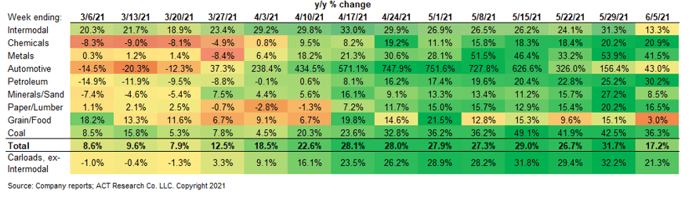

Since the strong rebound early in March from the polar vortex, rail trends have continued modestly above normal seasonal patterns, but Q2’21 acceleration in the y/y data below is mostly due to easier prior year comparisons.

In the latest two weeks in the table below, prior year comparisons were skewed by the timing of Memorial Day, which was a week earlier last year. The week ending June 5th was artificially depressed because it included the holiday this year but not last. Still, with comparisons beginning to firm, rail volumes in the coming weeks will likely look more like that first week of June than April and May.

In addition to strong demand and ongoing equipment supply chain shortages, the constrained driver market is a major factor in the freight market equation, and one where we see early signs of a trend change.

With enough time, we believe the cure for high prices is high prices.

ACT Research is a partner of Cass. Their subscription-based ACT Freight Forecast report provides data-driven predictions for the unique cycles in freight demand, capacity, and rates in each of the truckload, LTL, and intermodal markets over a three-year planning horizon. While taking seasonality into account, these econometric forecasts consider several crucial variables, including freight market conditions, macroeconomic conditions, inventory levels and supply side factors.