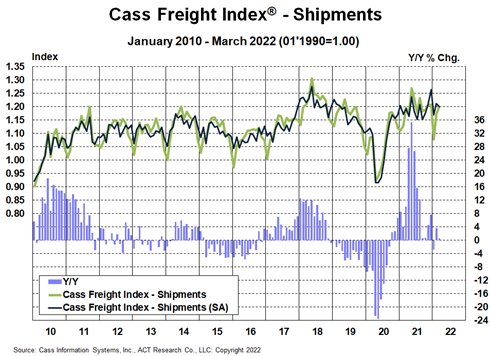

U.S. freight volumes slowed further in March, with the shipments component of the Cass Freight Index up just 0.6% y/y, slower than the 3.6% y/y growth in February.

See the methodology for the Cass Freight Index.

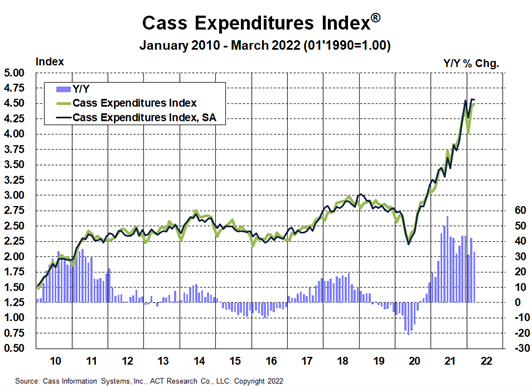

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, rose 1.1% m/m in March with shipments up 2.7% and rates down 1.6%. Year over year, freight expenditures were up 33% y/y.

This index rose 38% in 2021, after a 7% decline in 2020 and no change in 2019. Tougher comparisons in the coming months will naturally slow these y/y increases, but just using normal seasonality from here, the increase in 2022 will still be about 25%.

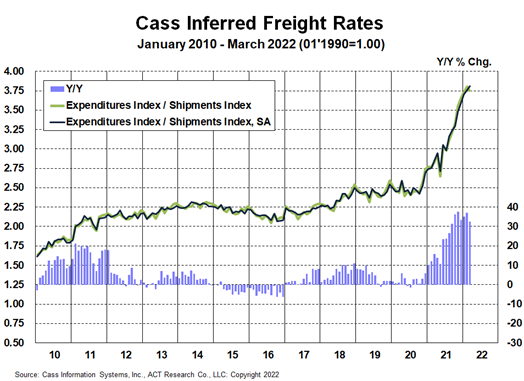

The freight rates embedded in the two components of the Cass Freight Index slowed to a 32% y/y increase in March from 37% in February.

The m/m increase is mainly as Omicron-related effects on capacity continue to push rates higher, which may continue to impact contract rates for a couple more months, even as downward pressure now emanating from the truckload spot market will have an increasing slowing effect over the course of the year.

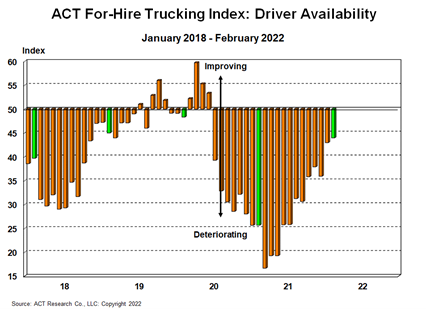

Though Class 8 tractor capacity remains limited and could tighten further if the Russia/Ukraine war worsens the chip shortage, we are seeing tangible signs of improvement in driver availability, which is disinflationary.

There have been tentative signs of recovering intermodal network fluidity, as chassis production continues to accelerate and workers return. But intermodal volumes continue to underperform the shipments component of the Cass Freight Index, so rail network congestion continues to add to Cass Inferred Freight Rates via excess miles in the freight network.

The true increase in freight costs is between the 14% y/y increase in the Cass Truckload Linehaul Index (below) and the 33% y/y increase in the inferred rate. The Truckload Linehaul Index does not include accessorial fees and rising fuel surcharges and does not consider excess miles. The inferred rate includes all costs across all modes.

After rising 23% in 2021, Cass Inferred Freight Rates are on a 23% trend again for 2022, though that seems unlikely to hold up.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data, expenditures divided by shipments, producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload representing more than half of the dollars, followed by LTL, rail, parcel, and so on.

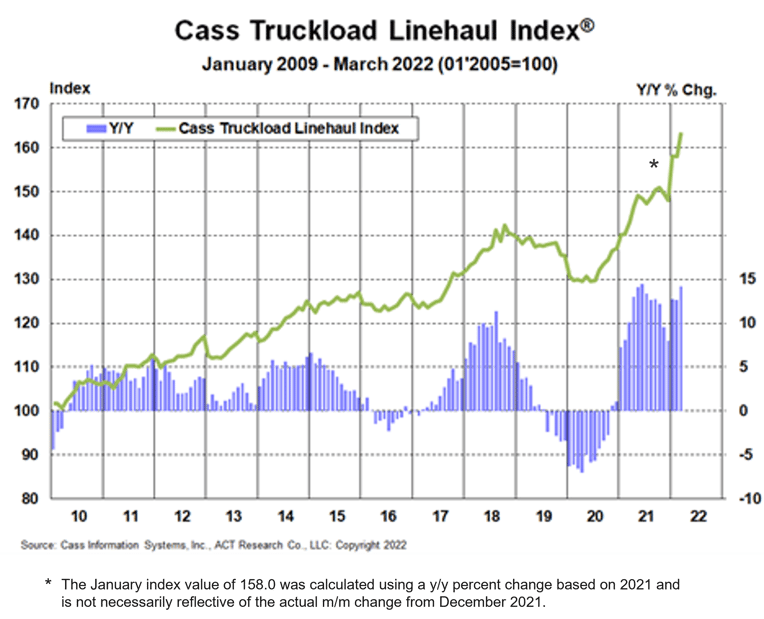

The Cass Truckload Linehaul Index® rose 14.2% y/y in March to 163.4 after rising 12.7% y/y in February to 158.0.

See the methodology for the Cass Truckload Linehaul Index.

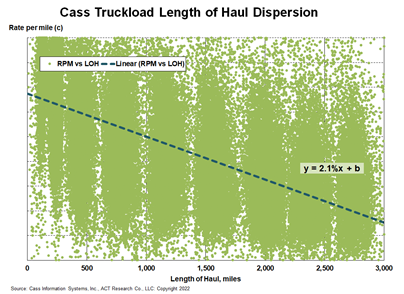

To demonstrate the effect of longer length of haul (LOH) on truckload rates, the scatter plot below analyzes a sample of 27 million truckload shipments in the Cass data set. This simple linear model that tells us that every 100-mile increase in LOH historically results in about a 2.1% lower rate per mile.

Our outlook for the U.S. freight market, detailed in the ACT Freight Forecast report, seems to have swung from below consensus to above consensus in the past several weeks, as we think recession fears are overdone.

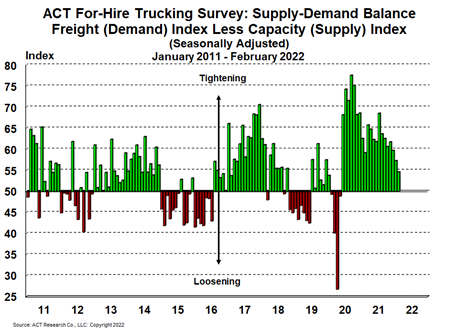

However, the pendulum has begun to swing. In early April, truckload spot rates inflected to y/y declines for the first time this cycle, but not the last. The ACT For-Hire Driver Availability Index has returned to levels where the rate turned down in late-2018 and 2019. Labor has recovered strongly from Omicron, which is deflationary for freight rates. Of course, spot rates are a leading indicator, so most of the effects of this change in the cycle will be felt further in the future.

In our view, the combination of inflation, Fed monetary tightening, war in Europe, and substitution back to services from goods are shifting the freight cycle from the early stage to the late stage.

The recovery in labor capacity is again a key feature, though equipment production remains constrained and marginal capacity entering the market by paying nearly new truck prices for three-year-old used trucks will have a high cost base and difficulty competing at lower spot rates.

Supply shortages may still tighten the truckload sector, depending particularly on neon, and will continue to have a big impact on the direction of the U.S. freight cycle. For now, there is a clear rebalancing happening, which should put us in the peak of the rate cycle.

If you rely on freight data to run your business, you may want to take a look at the ACT Freight Forecast report, which provides monthly predictions for the TL, LTL and intermodal markets, including capacity, volumes and rates, and forecasts for the shipments component of the Cass Freight Index and the Cass Truckload Linehaul Index through 2023.

Release date: We strive to release our indexes on the 12th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.