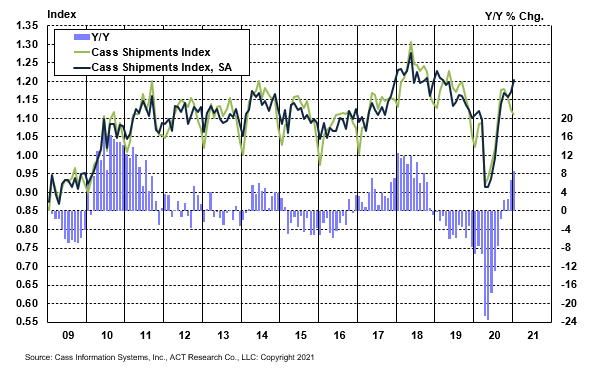

The shipments component of the Cass Freight Index accelerated to 8.6% y/y growth in January 2021 from 6.7% y/y growth in December. This was higher than the 7.8% predicted in this month’s ACT Freight Forecast report (an in-depth report written by this author). The 1.1% m/m drop from December was much less than normal seasonality; however, on a seasonally adjusted (SA) basis, the shipments index rose 3.0% m/m from December. This was the largest SA m/m increase since September. This acceleration takes us another step closer to the strong growth environment which we expect to continue in 2021, due in no small part to easy comparisons. On a two-year stacked basis, the Cass Shipments Index was still 1.6% below January 2019.

Chart: Cass Shipments Index, January 2009 – January 2021 (01’1990=1.00)

See the methodology for the Cass Freight Index.

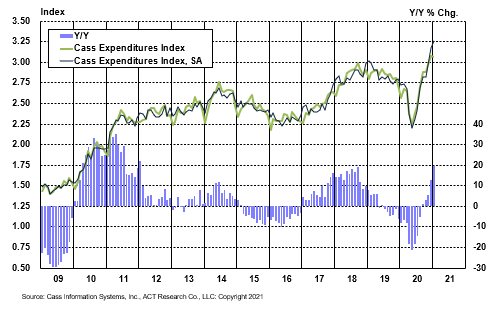

The strong acceleration in the Cass Expenditures Index continued in January to 19.5% y/y growth from 13.0% in December. The acceleration was driven primarily by volumes. Comparing the month-to-month changes in both shipment volumes and total dollars spent on freight, the expenditures index was up 2.8% m/m on a seasonally adjusted basis, while the shipments index was up almost the same amount (3.0% m/m SA). Freight rate increases accelerated in January at the fastest pace since 2009-2011, with the exception of a few months in late 2018. As these higher volumes meet rising contract rates, it is clear that this index is headed for growth rates over the next several months not seen since 2010-2011.

Chart: Cass Expenditures Index, January 2009 – January 2021 (01’1990=1.00)

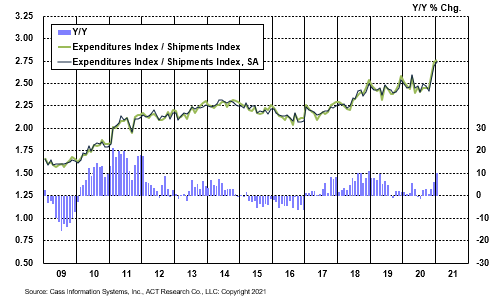

A simple calculation of the Cass Freight Index data (expenditures divided by shipments) produces a data set of “implied freight rates” that explains the overall movement in rates. The freight rates embedded in the Cass Freight Index accelerated to a 10.1% y/y increase in January from a 6.0% y/y increase in December. The acceleration reflects the fact that some contract rates adjust at the start of the calendar year. Last year the renewals were generally at lower rates, and this year the situation is quite the contrary. This data series is diversified among all modes, with truckload representing more than half of the dollars, followed by rail, LTL, parcel, and so on.

Chart: Cass Implied Freight Rates, January 2009 – January 2021 (01’1990=1.00)

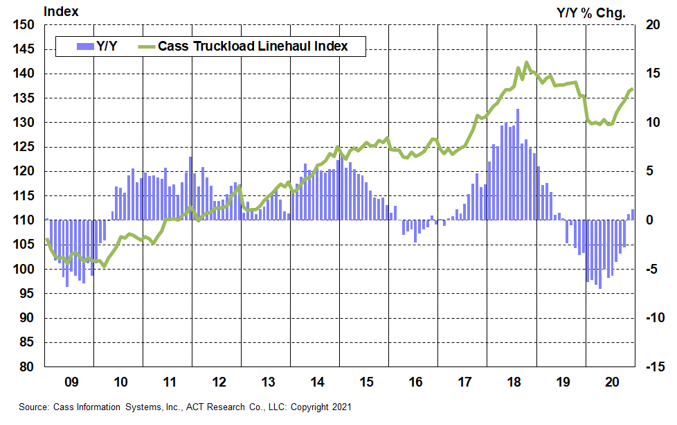

In January, the Cass Truckload Linehaul Index®, which measures per-mile linehaul rates independent of fuel and accessorials, accelerated significantly to a 7.3% y/y increase, after a 1.1% y/y increase in December. Consistent with the Cass Implied Freight Rates series, the acceleration came from both m/m improvement and an easier prior year comparison. On a m/m basis, the seasonally adjusted index rose 2.3% in January, and has now risen for seven straight months for a total gain of 8.1% since June.

Although there has been some slowing in spot rates and consumer spending recently, capacity remains tight. Microchip shortages present large challenges for manufacturers working to raise auto and truck production. With additional federal stimulus likely to drive more consumer spending; lean inventories; and a long backlog of ships at U.S. ports, we expect the Cass Truckload Linehaul Index to continue to improve in the near-term.

Chart: Cass Truckload Linehaul Index®, January 2009 – January 2021 (01’1990=1.00)

See the methodology for the Cass Truckload Linehaul Index.

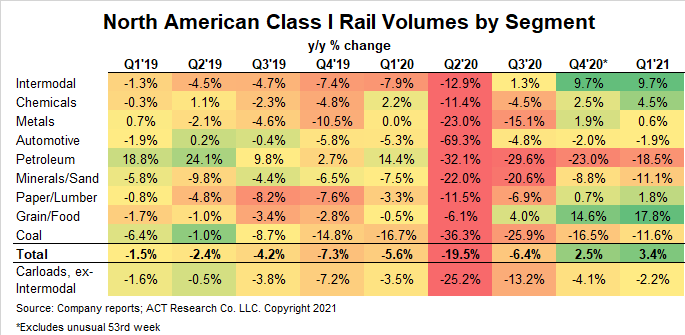

The improvement in the Cass Shipments Index is consistent with the generally improving trends in the railroad sector, where intermodal volumes had a very strong finish to 2020 and start to 2021. In our estimation, the slower rail volume trends in recent weeks partly reflect U.S. port constraints, as long lines of ships wait to unload but turn times are extended by labor shortages due to rising dockworker COVID infection rates. Freight demand is clearly still strong, but there is significant near-term risk that truck manufacturers will not be able to meet that demand from parts shortages in semiconductors, steel, and likely other parts stuck on those containerships.

We continue to forecast very strong GDP growth this year with more stimulus on the way in the coming weeks. While we expect rising vaccination rates to become a headwind to freight demand over time as services resume, the near-term outlook for freight demand remains extraordinarily strong.

The microchip shortage is acutely affecting auto and truck production, which is reducing freight volumes from the supply side and limiting the industry’s ability to manufacture the equipment needed to relieve the capacity tightness. This is likely to continue well into the second quarter.

To address a frequently asked question of late, we do not expect 2021 to repeat the significant rate relief shippers experienced in 2019. The ACT Freight Forecast report provides much more detail on the timing of the market rebalancing and eventual relief.