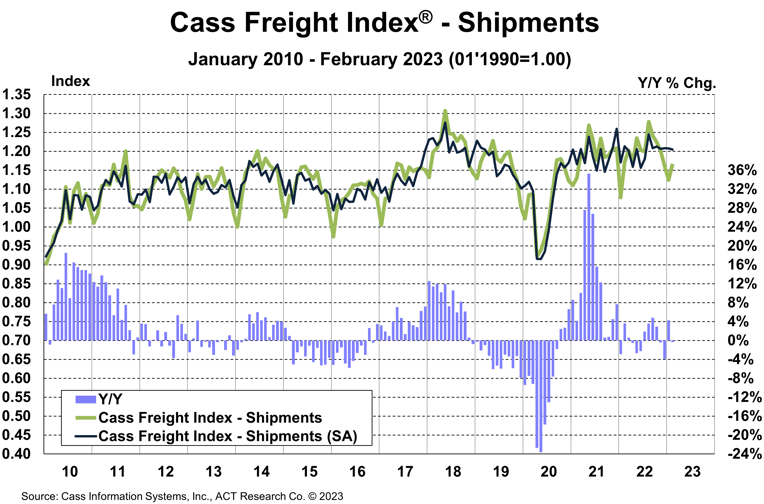

The shipments component of the Cass Freight Index® rose 3.8% m/m in February after a 3.2% m/m decline in January.

There has been a considerable increase in the proportion of truckload (TL) freight over the past several months, amid declines in less-than-truckload (LTL) and intermodal volumes. This suggests freight is migrating to TL from other modes, which fits with the robust growth in truckload capacity metrics, which have hardly started to slow at this point.

See the Methodology for the Cass Freight Index

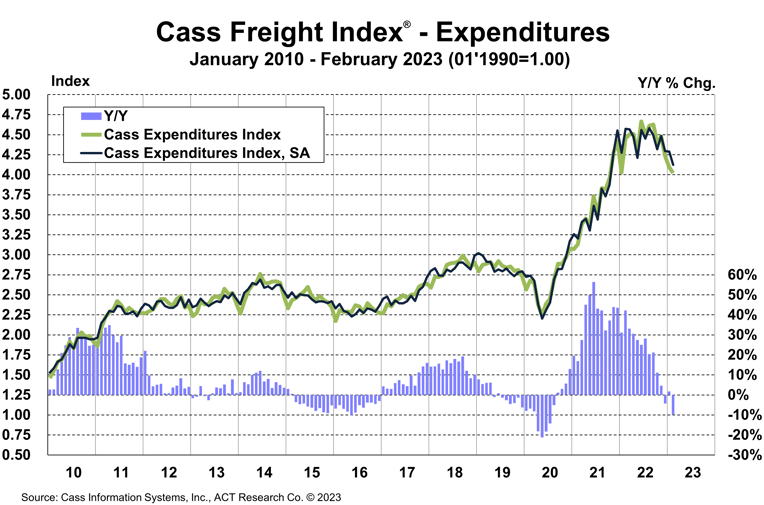

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, fell 1.9% m/m in February, and on some volatile comparisons fell to a 9.7% y/y decline after a 1.7% y/y increase in January.

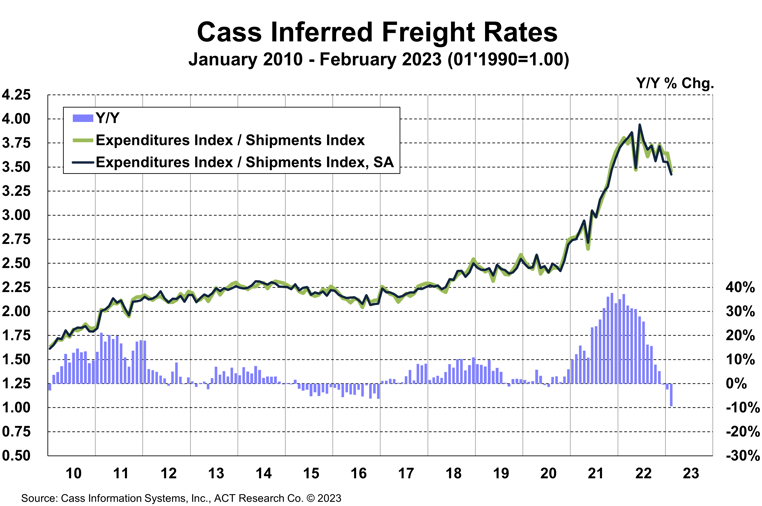

Looking at the m/m changes, with shipments up 3.8% but total expenditures down, we infer that rates were down 5.5% m/m (see our inferred rates data series below).

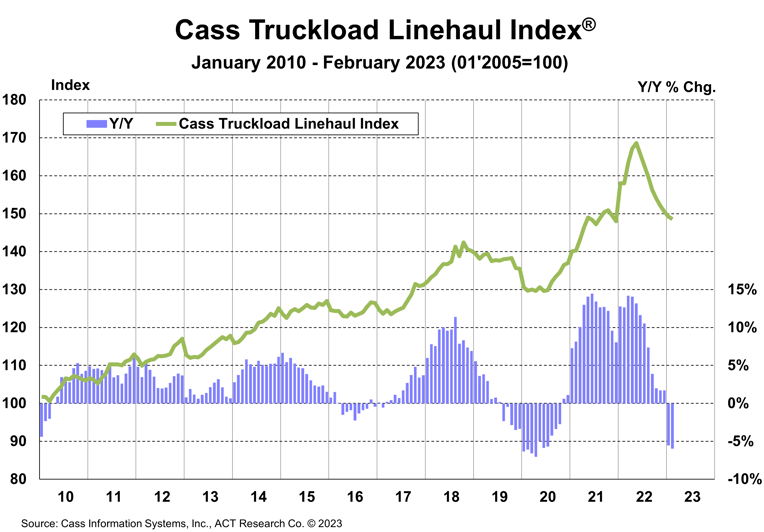

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index.

The expenditures component of the Cass Freight Index rose 23% in 2022, after a record 38% increase in 2021, but is set to retrench in 2023.

The rates embedded in the two components of the Cass Freight Index declined 9.4% y/y in February, after falling 2.4% in January.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index® fell 0.4% m/m in February to 148.6, after a 0.9% m/m decline in January.

See the Methodology for the Cass Truckload Linehaul Index

At the risk of stating the obvious, the fundamental reason truckload spot rates are still falling is there are too many drivers chasing too little freight. But the freight market is constantly dynamic, and we expect current loose conditions to first rebalance and then tighten over the course of the next year or so.

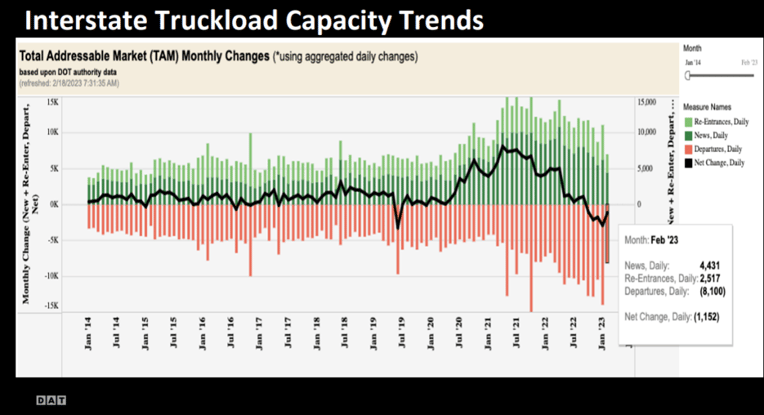

The truckload driver population has nearly stopped growing, and we think it will start to contract soon. The Bureau of Labor Statistics (BLS) trucking employment has already slowed to a 0.3% annualized rate in the seven months through February. In the spot market, capacity has already started to contract as carrier failures have accelerated, as shown in the chart below, assembled by our partners in freight analysis at DAT.

In Q4’22, net failures using Department of Transportation (DOT) interstate operating authority data (plus TX and CA intrastate, as there are long-haul routes within those two states), show an exit rate of about 2,000 net departures per day, though it has slowed recently.

ACT's DOT captures a broader market than truckload freight, so we can’t fully extrapolate this to TL capacity, but it is a great directional indicator of spot capacity. The decline in DOT operating authorities that started in October 2022 is evidence that the bottoming process is progressing.

While the industry has already removed more capacity than in prior downcycles by this measure, we think there is a migration from small fleets to larger, steadier fleets happening. This also suggests we shouldn’t over-extrapolate this data to TL capacity, but it is THE canary in the coalmine. Spot capacity is contracting, which is key to the ongoing bottoming process of the spot rate cycle.

For more on the future direction of freight markets, the ACT Research Freight Forecast provides analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type. The service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast is released monthly in conjunction with this report.

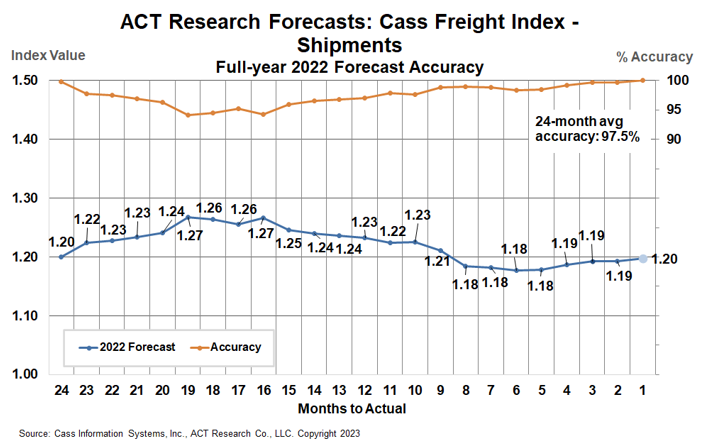

So how have their forecasts performed? For 2022, ACT’s forecasts for the shipments component of the Cass Freight Index were 97.5% accurate on average for the 24-month forecast period. The January 2021 forecast, two full years out, was 99.8% accurate.

(As a reminder, ACT Research’s Tim Denoyer writes this report for Cass.)

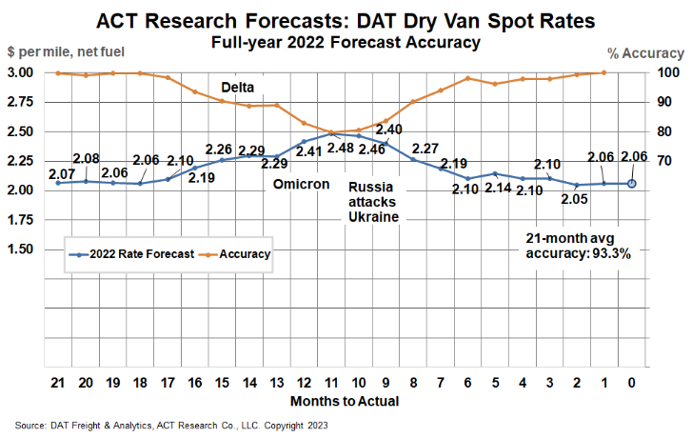

ACT's full-year 2022 DAT spot rate forecasts were 99.7% accurate from Q2’21 (19-21 months out) for dry van and 98.5% for reefer. DAT dry van spot rates, net fuel, finished 2022 at $2.06 per mile, in line with our forecasts to the penny from 18 and 19 months out (June and July 2021).

For more on the future of freight markets, the ACT Research Freight Forecast provides analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type. The service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast is released monthly in conjunction with this report.

Release date: We strive to release our indexes on the 12th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.