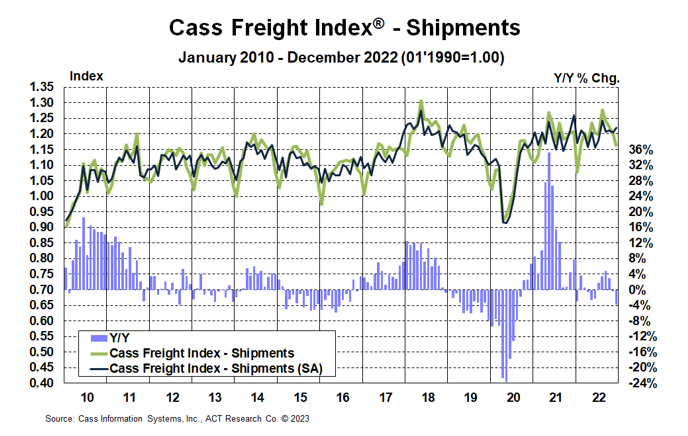

The shipments component of the Cass Freight Index® fell 3.9% y/y in December. On a m/m basis, the index fell 3.3%, but seasonality boosts December’s m/m performance to a 1.2% gain on an SA basis.

Normal seasonality from here would have shipments back in positive territory y/y in 1H’23, but sharpening declines in imports, into the West Coast in particular, suggest near-term trends may soften further.

See the methodology for the Cass Freight Index.

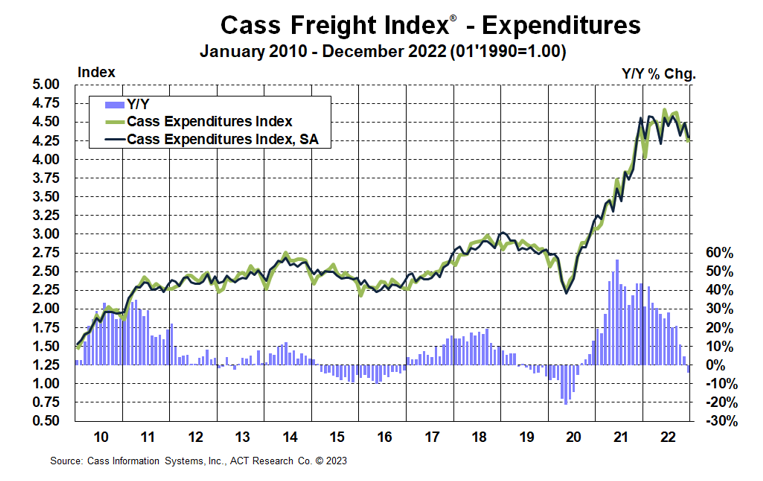

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, fell 4.3% y/y in December, inflecting from a 4.7% increase in November.

Expenditures fell 5.5% m/m after a 1.8% increase in November. Against a shipment decline of 3.3% m/m in December, we infer rates were down 2.2% (see our inferred rates data series below). The decrease in rates m/m seems mainly due to lower truckload contract rates.

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index rose 23% in 2022 after a record 38% increase in 2021 but is set to retrench in 2023.

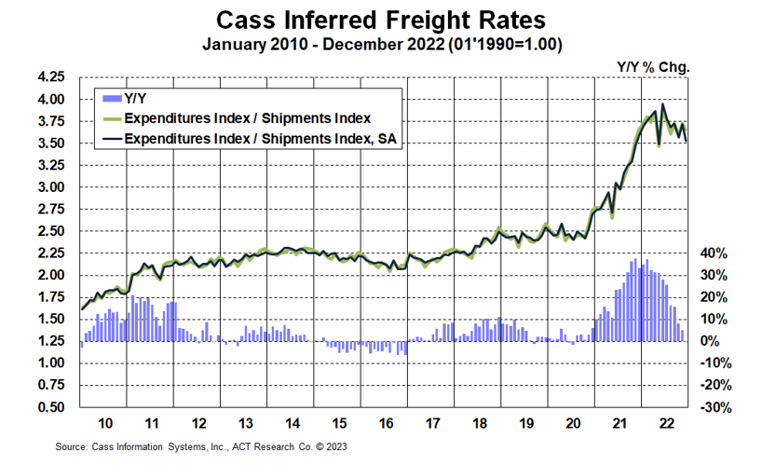

The rates embedded in the two components of the Cass Freight Index turned to a 0.4% y/y decline in December, after 5.1% y/y growth in November.

Freight rates are on track to fall 5% in 2023 just based on the normal seasonal pattern of this index. With loose market conditions and some welcome relief in diesel prices, the actual decline is likely to be a good bit larger.

Along with sharp declines in ocean rates and many commodity prices, lower freight costs aid the outlook for significant disinflation needed to improve economic conditions.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

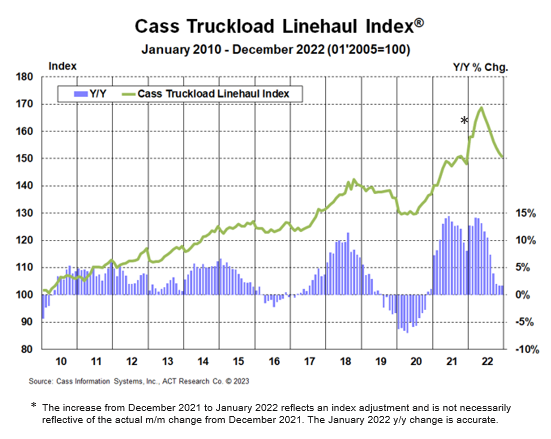

The Cass Truckload Linehaul Index fell 1.0% m/m in December to 150.5, after a 1.2% m/m decline in November.

See the methodology for the Cass Truckload Linehaul Index.

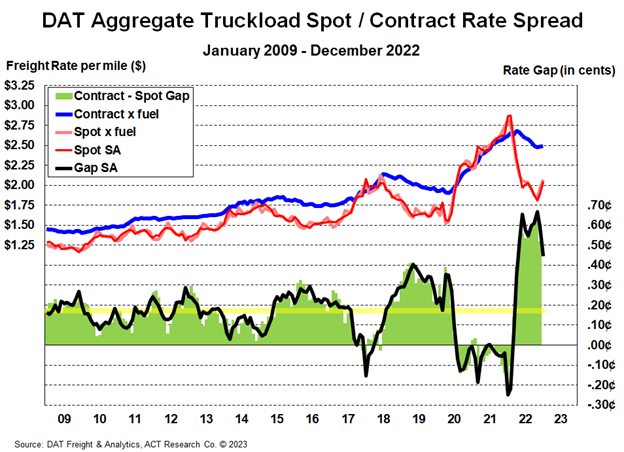

As we enter 2023, we see the truckload market transitioning from the late-cycle stage to the bottoming stage. Some of the recent rise in spot rates, ex-fuel, is due to seasonality, as rates surged toward the end of peak season, and some of it is the 70¢ per gallon drop in diesel prices in the past two months. Those gains tend to be competed away in loose markets like 2022 within a few weeks but have held so far.

After a long downtrend in 2022, the recent bounce in spot rates and tightening in the spot/contract spread suggest a bottoming truckload rate cycle. This should turn the trajectory of freight markets in 2023, and the cycle is likely to enter yet another phase later in 2023.

One exciting feature of the new freight data partnership between ACT Research and DAT Freight & Analytics is that it helps us (ACT Research) elaborate on the truckload rate environment. In particular, we think the difference between spot and contract rates, or the spread, is very instructive for the near-term direction of contract rates in particular.

From the large spread, there is downward pressure on contract rates, which has been the case for much of the past year. But we also see the recent tightening of that spread as a key signpost of this new stage of the cycle, even green shoots of a new rate cycle.

For more on why this is happening and what it means for the future of freight markets, the ACT Research Freight Forecast provides analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type. The service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast is released monthly in conjunction with this report.

Release date: We strive to release our indexes on the 12th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.