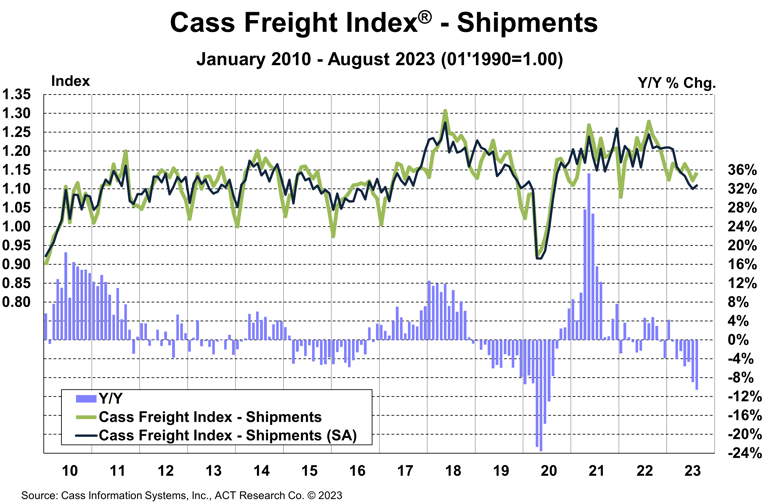

The shipments component of the Cass Freight Index® rose 1.9% m/m in August, or 0.8% m/m seasonally adjusted (SA).

The U.S. economy is accelerating, with the Atlanta Fed’s GDPNow tracking at 4.9% q/q GDP growth for Q3, driven by consumption. Though the resumption of student loan payments will likely trim this growth, real retail sales declines are moderating, and destocking seems to be mostly running its course.

With this backdrop, how are for-hire freight volumes declining so much? Private fleet growth is evident as Class 8 tractor retail sales are on pace to set a record this year, yet for-hire fleets are by and large demonstrating capital discipline. Thus, we think a substantial part of the decline in shipments is due to private fleets insourcing freight from the for-hire market.

With normal seasonality, this index would be flattish m/m in September and decline about 8% y/y, with still extraordinary comparisons, if less so.

See the Methodology for the Cass Freight Index

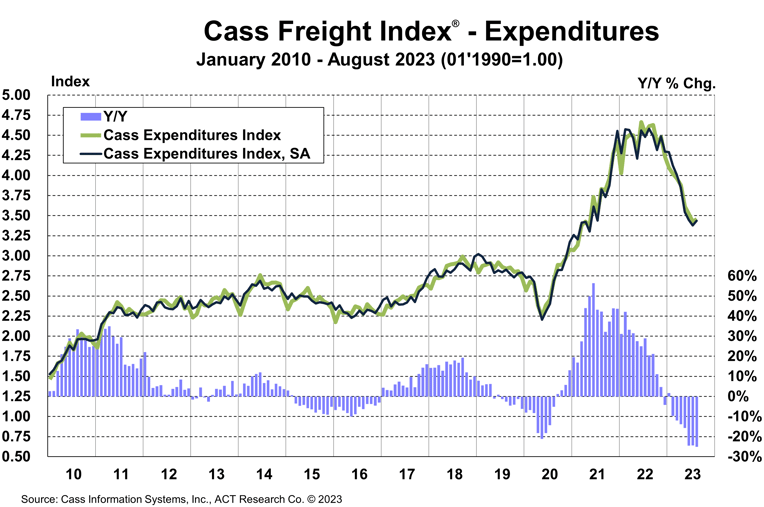

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, rose 1.1% m/m and fell 25.0% y/y in August.

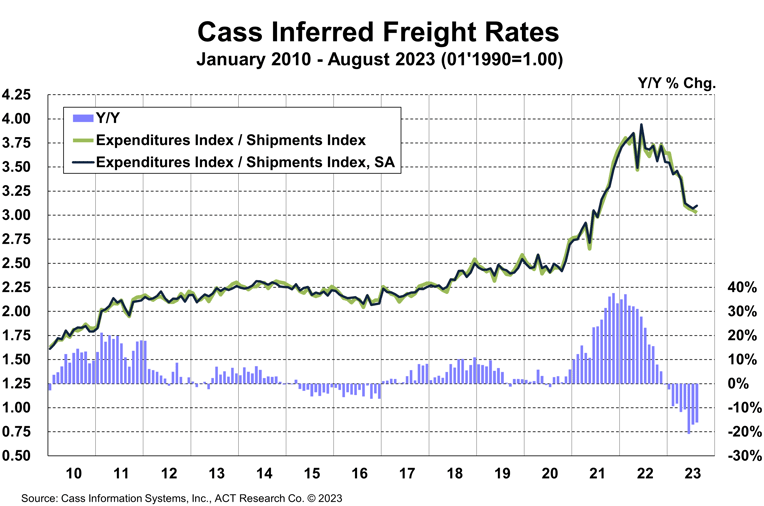

With shipments up 1.9% m/m in August, we infer rates were down 0.8% m/m (see our inferred rates data series below).

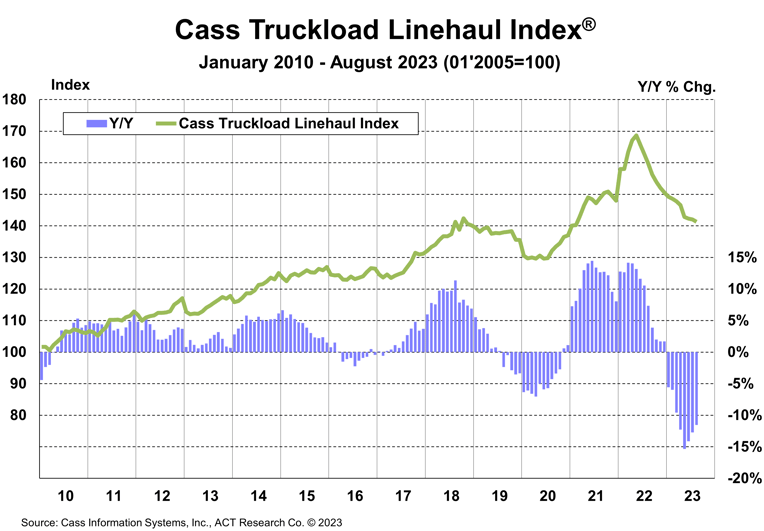

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index rose 23% in 2022, after a record 38% increase in 2021, but is set to decline about 18% in 2023 and 11% in 1H’24, assuming normal seasonal patterns from here. Both freight volume and rates remain under pressure at this point in the cycle, but fuel price increases could limit the savings for shippers.

The rates embedded in the two components of the Cass Freight Index declined 16% y/y in August, after falling 17% in July.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index® fell 0.5% m/m in August to 141.3, after a 0.2% m/m decline in July.

See the Methodology for the Cass Truckload Linehaul Index

Though significant progress has been made in rebalancing, we think it’s unlikely that industry capacity will broadly tighten until pressure from private fleet growth eases, which seems possible in the next few months.

Though the freight market is still near the bottom of the cycle, the first step in getting out of a hole is to stop digging. In our view, new truck orders in the next few months will be pivotal to setting the market tone for 2024.

The capacity contraction in the for-hire sector is beginning to coil the proverbial spring for better market conditions, but this improving outlook could be spoiled if fleet expansion continues ahead of industry need.

We expect industry financial trends to dictate greater capital discipline next year, but further overexpansion is possible as fleets plan for significant emissions regulations looming in the future.

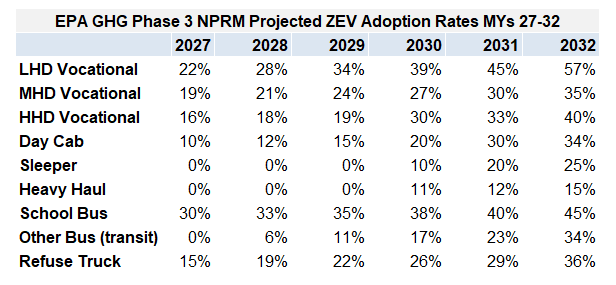

For example, the Notice of Proposed Rulemaking (NPRM) for the EPA’s upcoming greenhouse gas (GHG) regulation includes the targets for adoption rates of zero-emissions vehicles (ZEVs), as shown in the table below. This could have major implications for industry capacity.

If you need to understand the future direction of freight markets, the ACT Research Freight Forecast provides in-depth analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type, LTL and intermodal price indexes. This service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast is released monthly in conjunction with this report.

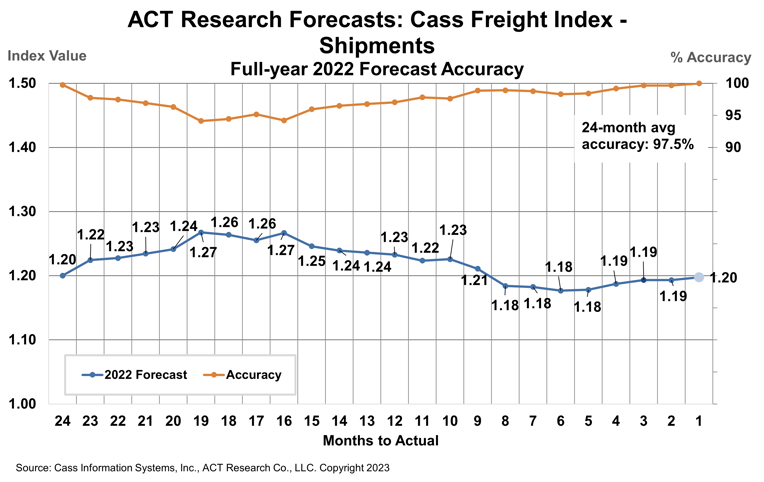

How have their forecasts performed? For 2022, ACT’s forecasts for the shipments component of the Cass Freight Index were 97.5% accurate on average for the 24-month forecast period. Our January 2021 forecast, two full years out, was 99.8% accurate.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

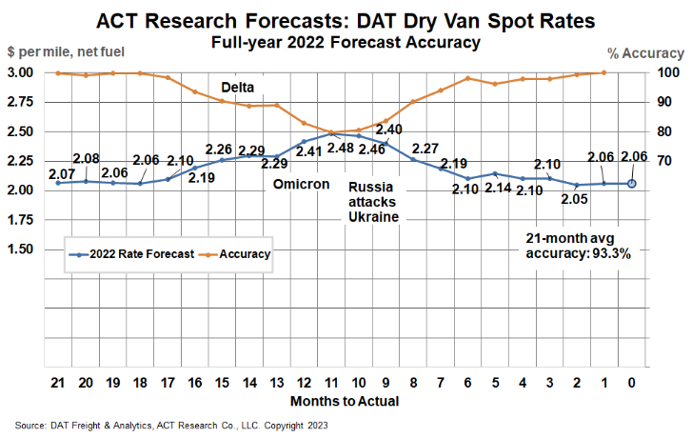

ACT Research’s full-year 2022 DAT spot rate forecasts were 99.7% accurate from Q2’21 (19-21 months out) for dry van and 98.5% for reefer. DAT dry van spot rates, net fuel, finished 2022 at $2.06 per mile, in line with our forecasts to the penny from 18 and 19 months out (June and July 2021).

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.