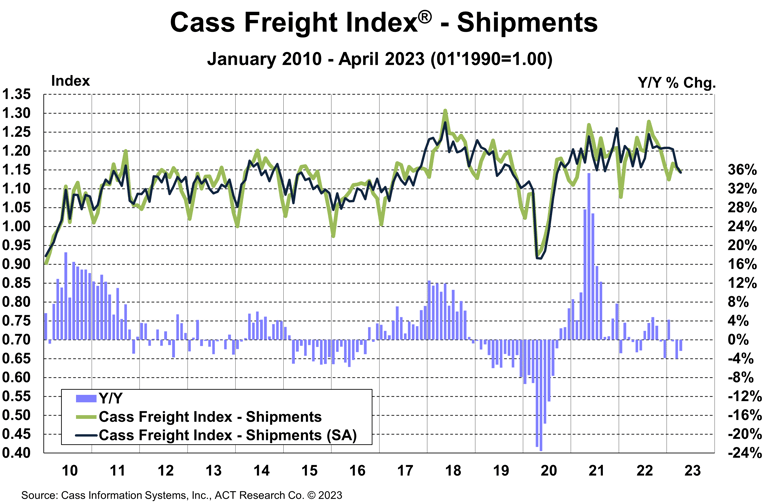

The shipments component of the Cass Freight Index® fell 2.4% y/y in April as freight markets remain muted and continue to work through an extended soft patch.

Declining real retail sales trends and ongoing destocking remain the primary headwinds to freight volumes, but dynamics are shifting as real incomes are improving, and the worst of the destock is most likely in the rearview.

Normal seasonality from the April index level suggests 1%-3% y/y declines for the next few months.

See the Methodology for the Cass Freight Index

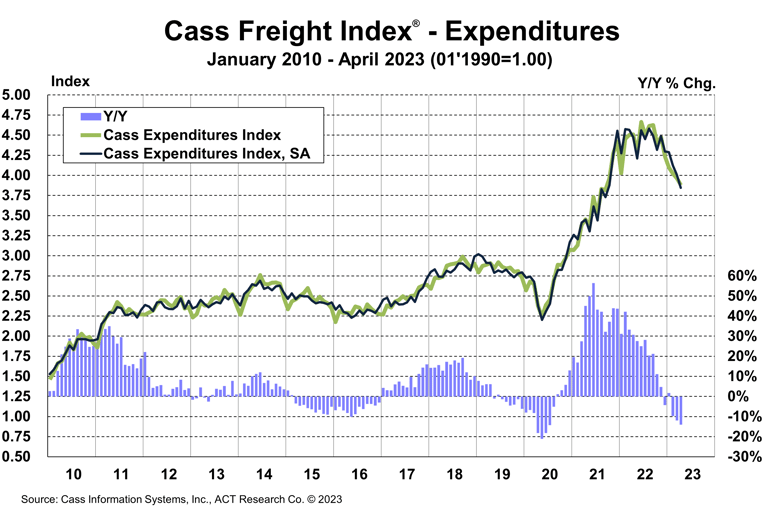

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, fell 2.1% m/m and 14.0% y/y in April.

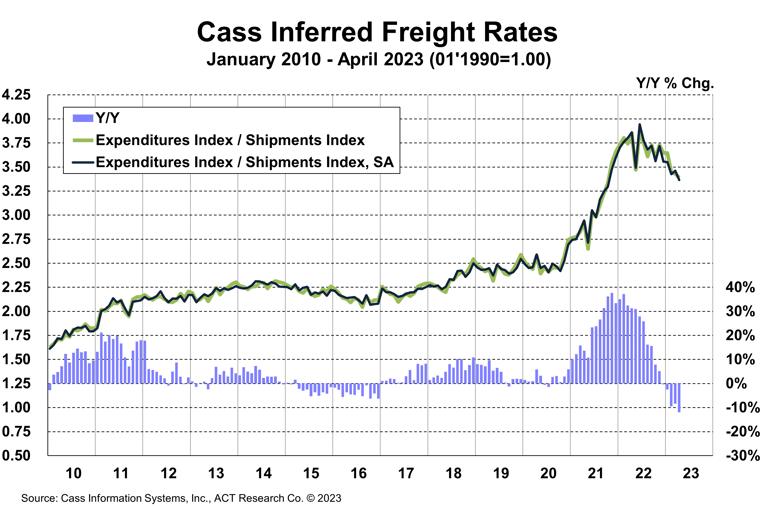

With shipments down 1.0% m/m in March, we infer rates were down 1.2% m/m (see our inferred rates data series below).

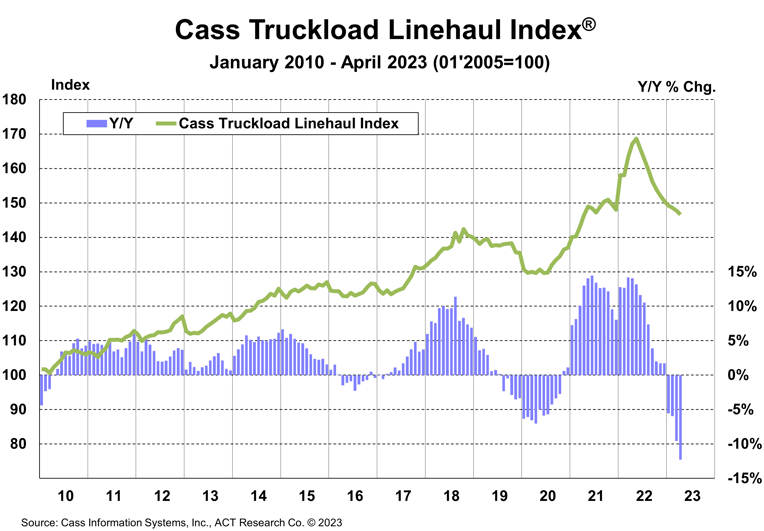

This index includes changes in fuel, modal mix, intramodal mix, and accessorial charges, so is a bit more volatile than the cleaner Cass Truckload Linehaul Index®.

The expenditures component of the Cass Freight Index rose 23% in 2022, after a record 38% increase in 2021, but is set to decline about 12% in 2023, assuming normal seasonal patterns from here.

The rates embedded in the two components of the Cass Freight Index declined 11.9% y/y in April, after falling 8.3% in March.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data—expenditures divided by shipments—producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload (TL) representing more than half of the dollars, followed by less-than-truckload (LTL), rail, parcel, and so on.

The Cass Truckload Linehaul Index, which measures changes in linehaul rates, fell 0.8% m/m in April to 146.6, after a 0.6% m/m decline in March.

See the Methodology for the Cass Truckload Linehaul Index

When conditions will improve is a topic largely reserved for ACT Freight Forecast subscribers. But after a long soft patch, we see the U.S. freight transportation industry on the verge of a new cycle as we begin to transition from the bottoming phase into the early phase of the freight cycle in the months to come.

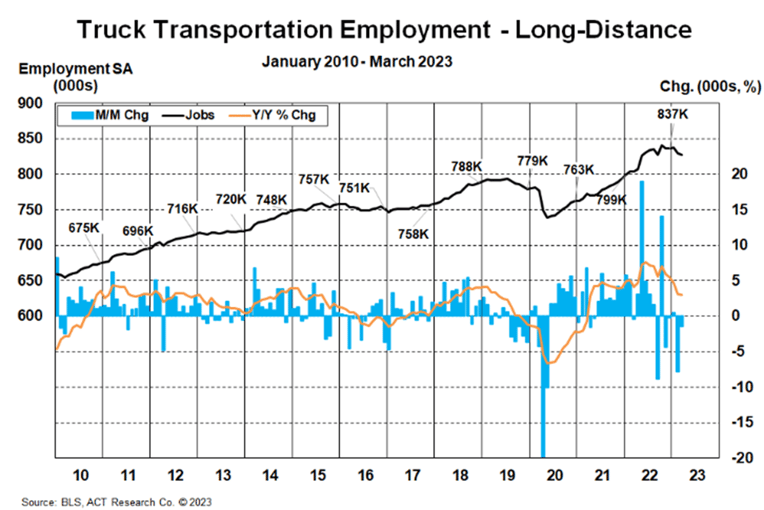

Of course, demand recovery is an important part of the outlook, but supply trends are shifting as well. Although new equipment production is elevated, we estimate DOT operating authorities have been declining for about seven months now, and employment is broadly following suit.

Though the total trucking employment data series rose by 3,000 jobs in April, March was revised down by 2,500 jobs, leaving little net change. However, the long-distance trucking employment series is telling a different story, and this series is more tightly related to truckload freight markets.

In contrast to the 5,400-job increase in total trucking employment so far this year through April (+2,400 in Q1), long-haul trucking jobs declined by 8,700 jobs in Q1’23, or 1.0%, as shown in the chart. While still up 3.0% y/y in that latest March data point, the series will be down on a y/y basis by June on its current level. Since trends in employment follow trends in freight rates, long-haul jobs are set to decline this year.

For more on the future direction of freight markets, the ACT Research Freight Forecast provides analysis and forecasts for a broad range of U.S. freight measures, including the Cass Freight Index, Cass Truckload Linehaul Index, and DAT spot and contract rates by trailer type. The service provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets over a two- to three-year time horizon, including capacity, volumes, and rates. The Freight Forecast is released monthly in conjunction with this report.

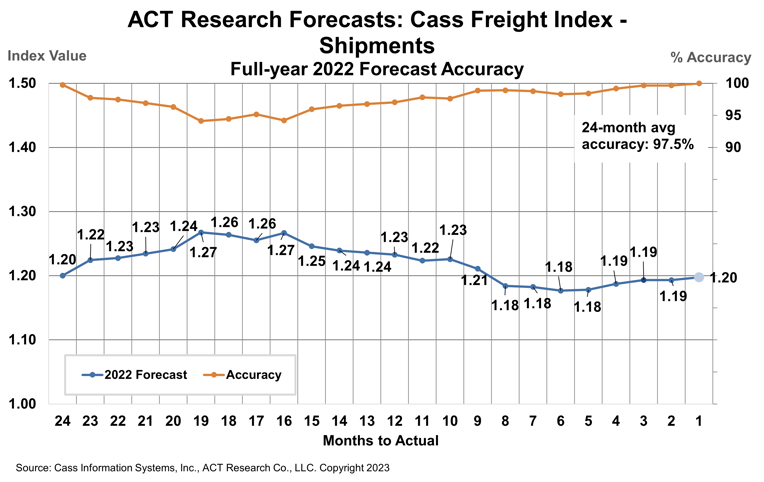

How have their forecasts performed? For 2022, ACT’s forecasts for the shipments component of the Cass Freight Index were 97.5% accurate on average for the 24-month forecast period. Our January 2021 forecast, two full years out, was 99.8% accurate.

(As a reminder, ACT Research’s Tim Denoyer writes this report.)

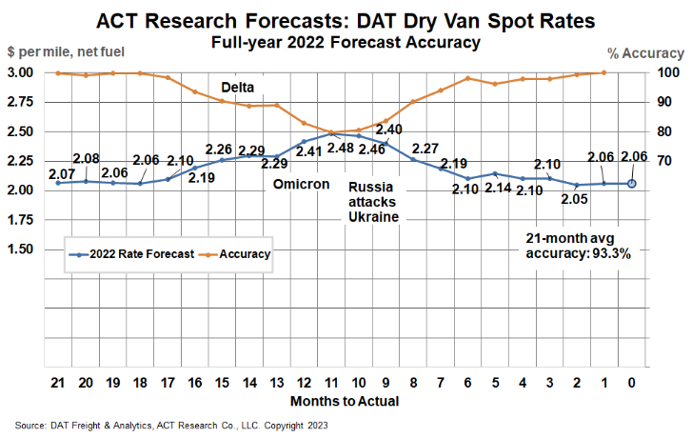

ACT Research’s full-year 2022 DAT spot rate forecasts were 99.7% accurate from Q2’21 (19-21 months out) for dry van and 98.5% for reefer. DAT dry van spot rates, net fuel, finished 2022 at $2.06 per mile, in line with our forecasts to the penny from 18 and 19 months out (June and July 2021).

Release date: We strive to release our indexes on the 13th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.