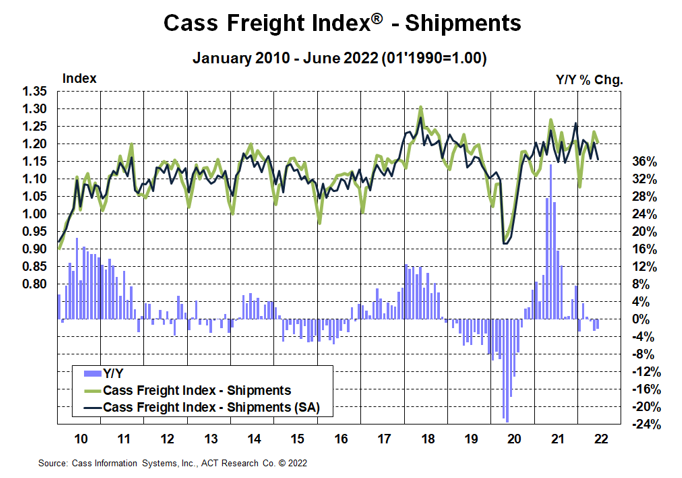

The shipments component of the Cass Freight Index® declined 2.3% on a y/y basis in June, similar to the 2.7% y/y decline in May. After the May result was slightly ahead of ACT Research’s estimate, the June result was slightly behind, but no big surprises.

Normal seasonality from this index level would imply shipments down 1% y/y in Q3 and down 5% y/y in Q4, as the current soft patch is becoming increasingly clear in the data.

See the methodology for the Cass Freight Index.

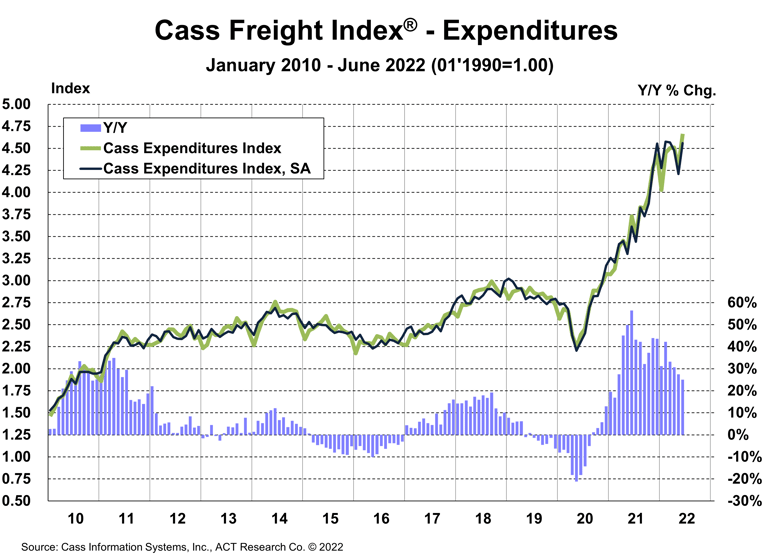

The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, rose 8.8% m/m in June to a new record, with shipments down 2.6% and rates up 11.7%. The m/m noise on rates is largely mix, and reversed a 9.8% decline last month, and just means there was more truckload in the mix in June and more less-than-truckload (LTL) in May.

We estimate roughly 10 percentage points of the y/y increase are currently due to fuel prices alone. As a reminder, this index includes changes in fuel, modal mix, intramodal mix (which affects length of haul), and accessorial charges.

Simply using normal seasonality from here, this index will still be rising y/y through 2022, ending with a 2% y/y increase in December, against a 32% y/y increase in 1H’22.

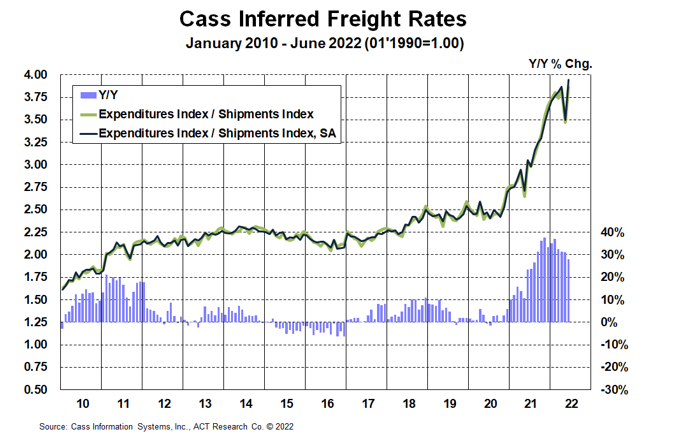

Cass Inferred Freight Rates, which measure the change in cost per shipment, still rose 28% y/y in June, decelerated from 31% y/y increase in May. Month to month, they rose 11.7% (12.9% SA), more than reversing the 9.8% decline in May (-9.5% SA).

The sequential increase was largely due to modal mix, as truckload moves (a higher cost per shipment) increased compared to LTL (lower cost per shipment), reversing the increase in LTL mix in May. Fuel prices also pushed rates up in June. And while underlying truckload rates started to pull back in June (see the Cass Truckload Linehaul Index, below), LTL rates continued to rise m/m.

The May decline in cost per shipment was also largely due to mix, as noted last month, and June freight rates were just 0.8% above April. We still see this as a leveling off of industry rates, with ongoing upward pressure from fuel even as the market balance has loosened this year and should begin to provide modest relief. This is subject in no small part to diesel prices, which have begun to drop, now down 24c over the past three weeks to a recent $5.57 per gallon according to the U.S. Energy Information Administration (EIA). The price of diesel remains well above where our simple regression with crude would suggest, reflecting a considerable war premium.

So, the familiar refrain is true, shippers aren’t feeling the savings from declining spot rates. Yet. At this point, it is increasingly oil prices in the way, but such relief is increasingly likely, which is welcome news for the broader inflation picture.

Cass Inferred Freight Rates are a simple calculation of the Cass Freight Index data, expenditures divided by shipments, producing a data set that explains the overall movement in cost per shipment. The data set is diversified among all modes, with truckload representing more than half of the dollars, followed by LTL, rail, parcel, and so on.

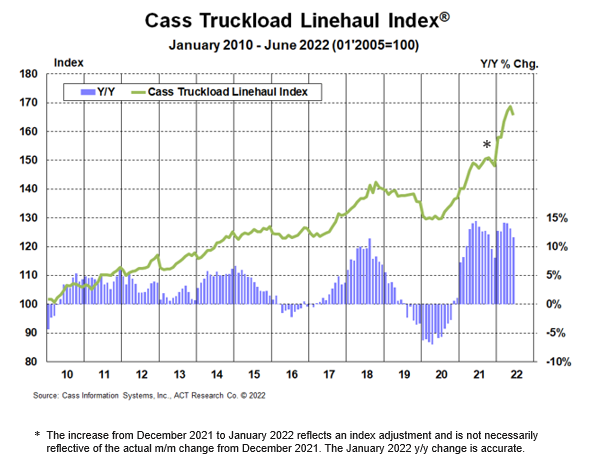

The Cass Truckload Linehaul Index® , which measures market fluctuations in per-mile truckload linehaul rates, independent of additional cost components such as fuel and accessorials, rose 11.6% y/y in June to 165.7 after rising 13.2% y/y in May.

See the methodology for the Cass Truckload Linehaul Index.

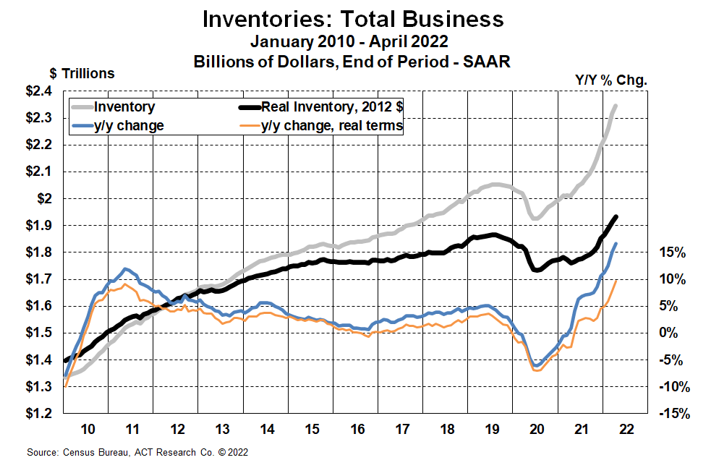

You may find a chart of inventories, one of the most lagged (toughest to calculate) monthly economic data series (with the latest numbers as of April), odd in the section about the outlook. But even from a few months ago, inventories provide key information about the future of the cycle. And we can say clearly that the current inventory levels do not bode well for freight demand.

Now that the pendulum has begun to swing, “how bad?” and “how long?” have become some of the most crucial questions. The ACT Freight Forecast report provides monthly, quarterly, and annual predictions for the TL, LTL, and intermodal markets, including capacity, volumes, and rates. The report provides monthly updates of forecasts for the shipments component of the Cass Freight Index® and the Cass Truckload Linehaul Index® through 2024, as well as DAT spot rates by trailer type, including and excluding fuel surcharges.

Release date: We strive to release our indexes on the 12th of each month. When this falls on a Friday or weekend, our goal is to publish on the next business day.